How I Raised My Credit Score While Collecting Credit Cards Like Pokémon

There’s a lot of chatter out there about how applying for too many credit cards will wreck your credit score. But, plot twist: it’s actually possible to boost your credit score while collecting credit cards—when you do it strategically. I've got a list of credit cards longer than the line for the bathroom at a concert, and yet, my credit score is sitting pretty at 836 (yeah, you read that right). The secret? It's all about being smart and responsible with how you use them.

Let’s break it down.

The Strategy Behind the Plastic

There’s a method to this madness. I don’t just apply for credit cards because I enjoy filling out applications (though that “You’ve Been Approved” screen is kinda thrilling). Here's when I apply:

1. Apply for Cards When You're Planning a Big Trip

Let’s be real, one of the best ways to rack up points is by signing up for credit cards right before a big trip. You know those sign-up bonuses that practically throw points at you? Apply for the cards that have killer bonuses. That’s how you make the most of your spending.

2. Chase Those Elevated Bonuses

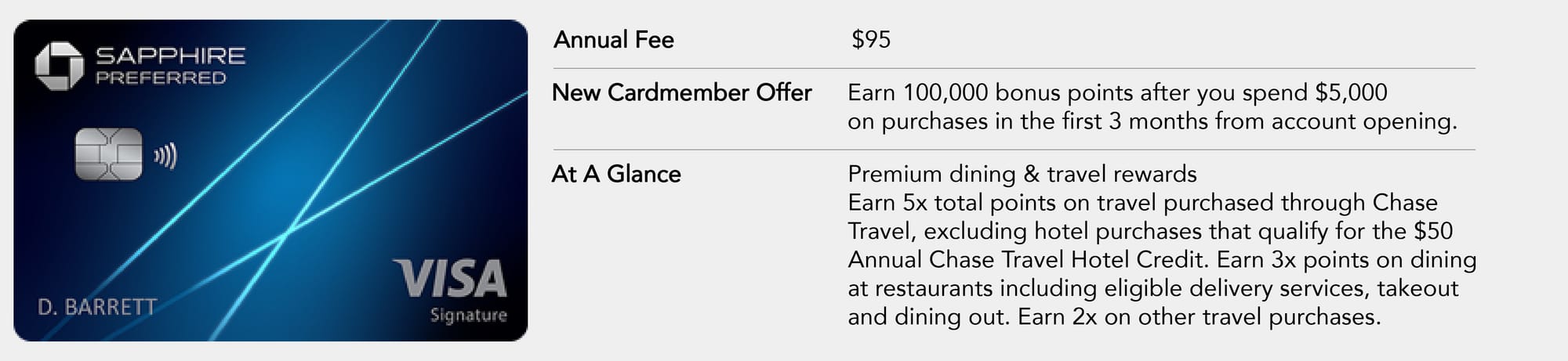

Sometimes, credit card companies throw out crazy-good bonus offers. If you’re lucky enough to find one, don’t let it pass you by. Higher sign-up bonuses = more points = more rewards for you. Chase Sapphire Preferred has a great one running right now!

3. Score Airline or Hotel Status

Certain cards come with perks like elite status with airlines or hotel chains. So, not only are you collecting points, but you’re climbing the status ladder, too. Imagine free upgrades or extra perks just for using your card responsibly. Yep, it’s that easy.

4. Maximize Spending in Each Category

Here’s the trick: not all credit cards are created equal. Each one has its own bonus categories. Use the best card for the job. Need groceries? Use the card with the highest grocery rewards. Traveling? Use the one that gives you travel perks. Simple as that.

The Responsibility Part (AKA Don't Be That Person)

This part is what actually helps your credit score. So pay attention, because it’s the not-so-secret sauce.

1. Always Pay Your Statement in Full

No one likes paying interest, right? Paying off your balance in full every month is like keeping your credit score in a happy place. It shows you’re responsible and doesn’t cost you a dime in extra fees.

2. Pay on Time (and Avoid Late Fees)

This is a no-brainer: late payments = credit score penalties. Set reminders, use autopay, or do whatever it takes to stay on top of it. Late payments are a quick way to kill your score.

3. Don’t Spend Just to Spend

We’ve all been tempted to go on a shopping spree because, hey, points! But don’t fall into that trap. Use your credit cards for things you were already going to buy—groceries, bills, regular expenses. Don’t stretch your budget just to rack up points.

Soft Pulls: The Credit Card Hack You Need to Know

Here’s a game plan that won’t hurt your score: apply for cards that let you check if you’re pre-approved through a soft credit pull. What’s the difference, you ask?

A soft pull happens when a lender checks your credit for pre-approval or you check your own score. No harm done.

A hard pull is when a lender reviews your credit because you’re applying for a card. Each hard pull knocks your score down a little, especially if you apply for too many cards in a short time.

Pro tip: Apply for cards with a soft pull pre-approval process. If you’re approved, go ahead and fill out the full application. This way, you know you’ve got a high chance of being accepted (90%+). It's like getting a backstage pass to credit card approval. Easy peasy.

Some Starter Cards That Don’t Totally Suck

If you’re looking to dip your toes into the credit card world, here are a few solid options:

Chase Sapphire Preferred

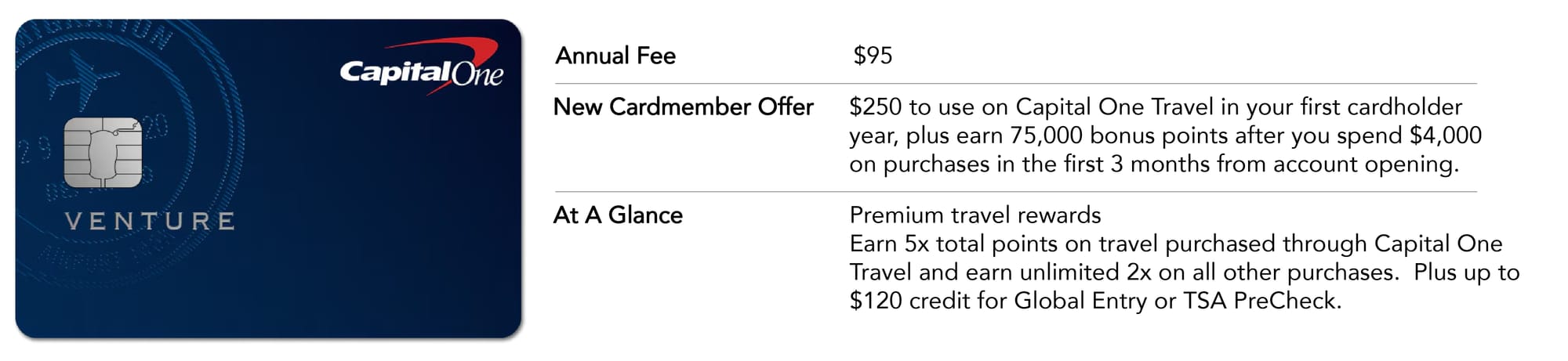

Capital One Venture Card

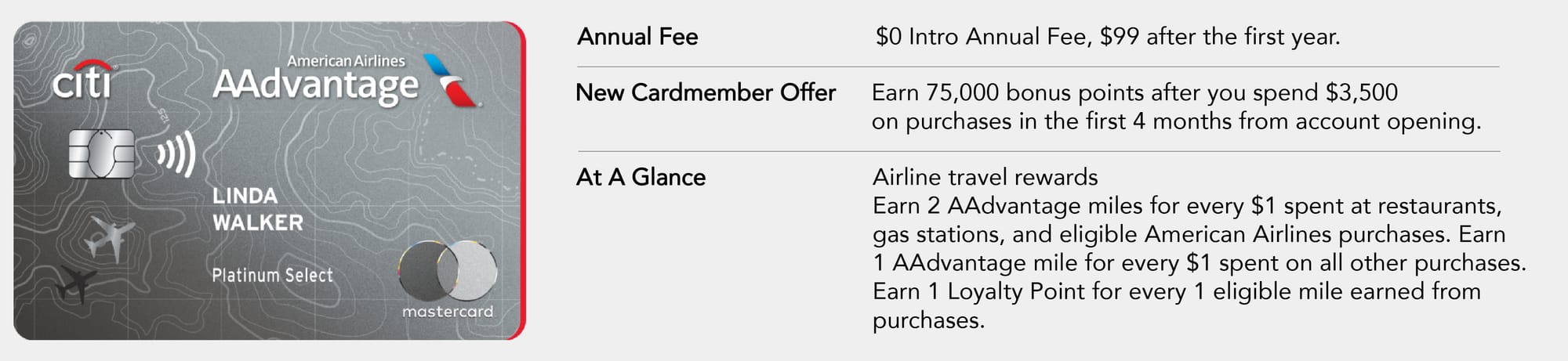

Citi AAdvantage Platinum Select World Elite Mastercard

This is a great option for a MasterCard to use with Plastiq 😉

**Some banks will require the pre-authorization request by phone.

Why Your Credit Score Loves (Smart) Credit Card Use

Let’s geek out for a sec. Your credit score is made up of a few key things:

📅 Payment History (35%) – Pay on time, and your score loves you.

💳 Credit Utilization (30%) – Keep balances low compared to your total available credit. Opening new cards increases your available credit, which can actually lower your utilization ratio. Win.

📜 Length of Credit History (15%) – The longer your accounts are open, the better. Don’t close your oldest cards unless they have crazy fees and offer you zero value.

📋 Credit Mix (10%) – Credit cards, car loans, mortgages. Having different types of credit helps.

🔍 New Credit (10%) – Too many new cards in a short time can raise eyebrows, but spread out your applications and you’re good.

Final Thoughts From Someone With Way Too Many Cards

So, can credit cards help your credit score? Absolutely. The key is being smart, strategic, and responsible. If you play your cards right (pun totally intended), you can increase your credit score, rack up travel rewards, and avoid the pitfalls of credit card debt. Just remember, it’s all about balance—use your cards wisely, pay on time, and don't go on a spree just to chase points.

Now if you’ll excuse me, I need to go put a flight to New York for Cherry Blossom season on the perfect 5x points card… and then pay it off like the responsible adult I pretend to be.

Note: Some links in this post may earn us a small commission at no extra cost to you, as we participate in affiliate programs. All information is accurate as of the date of publication but may change over time. Always check for the latest details before making travel plans.